Ontario iGaming market dips to five-month low in February

The regulated Ontario iGaming market bucked its trend of month-over-month growth in February, but both total wagering activity and operators’ gross gaming revenue are still well ahead of the pace the market was setting this time last year.

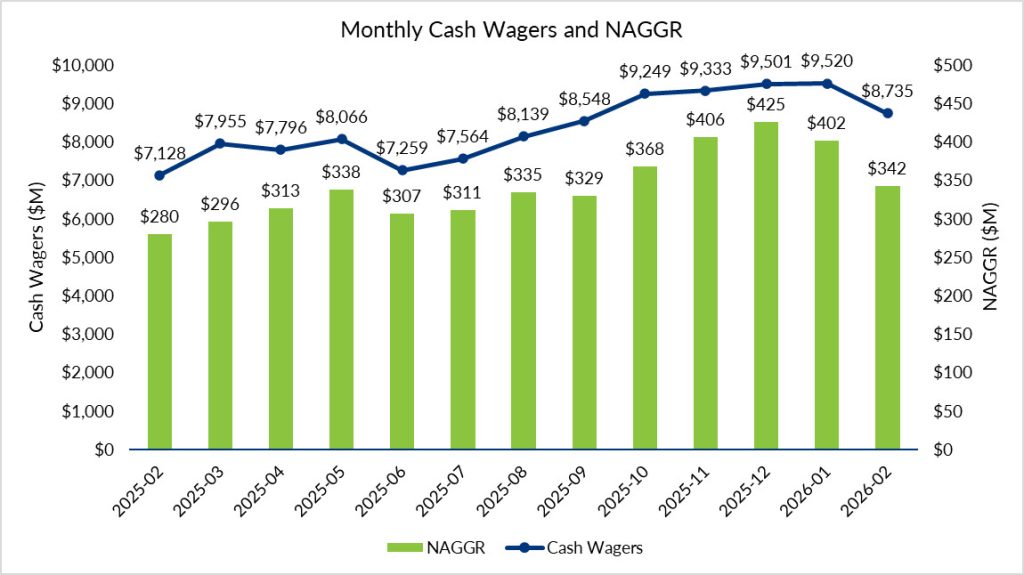

The latest iGaming Ontario (iGO) revenue report shows that the total value of cash wagers dropped 8% from an all-time monthly record of $9.52bn in January 2026 to $8.74bn in February. Non-adjusted gross gaming revenue (NAGGR) fell almost 15% from $401.5m to $342.4m.

Those February 2026 handle and revenue totals were both the lowest posted in a single month in the province since September 2025. Handle had eclipsed $9bn and NAGGR had beaten $400m in each of November, December, and January.

February, of course, has fewer days than any of those previous months. And the year-over-year trend for the month was strong: February 2026’s handle and revenue were each around 22% above February 2025, continuing the provincial regulated market’s consistent pattern of strong annual growth on a month-by-month basis as regulated Ontario iGaming nears the end of its fourth year.

Around 1.3 million player accounts were active last month, although the average revenue they yielded for operators was $264, the lowest monthly total since February 2025’s $248.

Ontario taxes operators at 20% of NAGGR, meaning the provincial government reaped around $68m in tax revenue from regulated iGaming in February.

Sports betting and iCasino’s differing fortunes continue

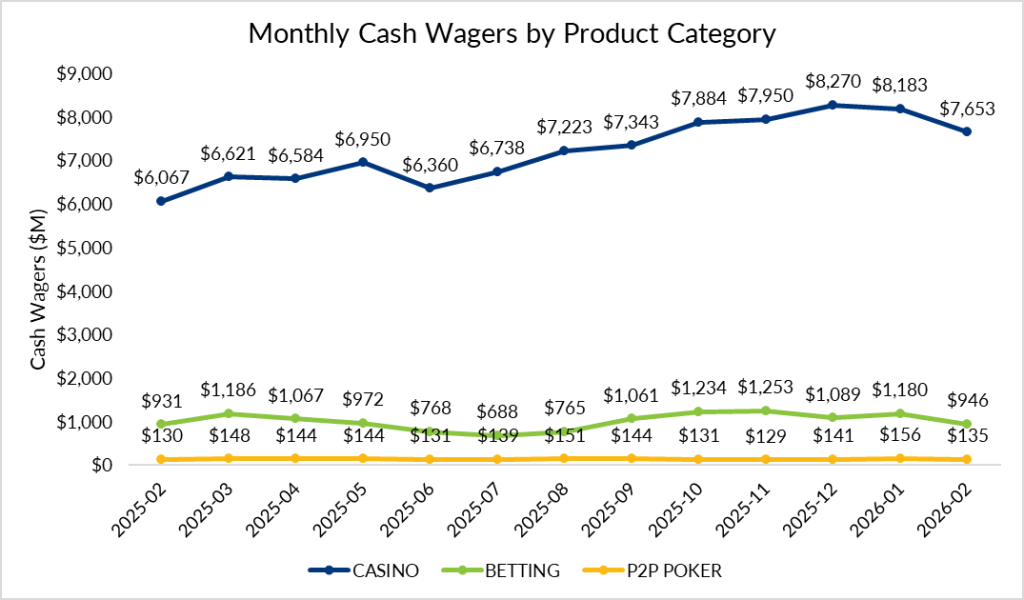

In a month that contained the favoured Seattle Seahawks beating the New England Patriots in a low-scoring Super Bowl LX, Ontario’s licensed sportsbooks took $946m in wagers, $15m (1.6%) more than they took in February 2025. That was Ontario’s lowest monthly sports betting handle since last August.

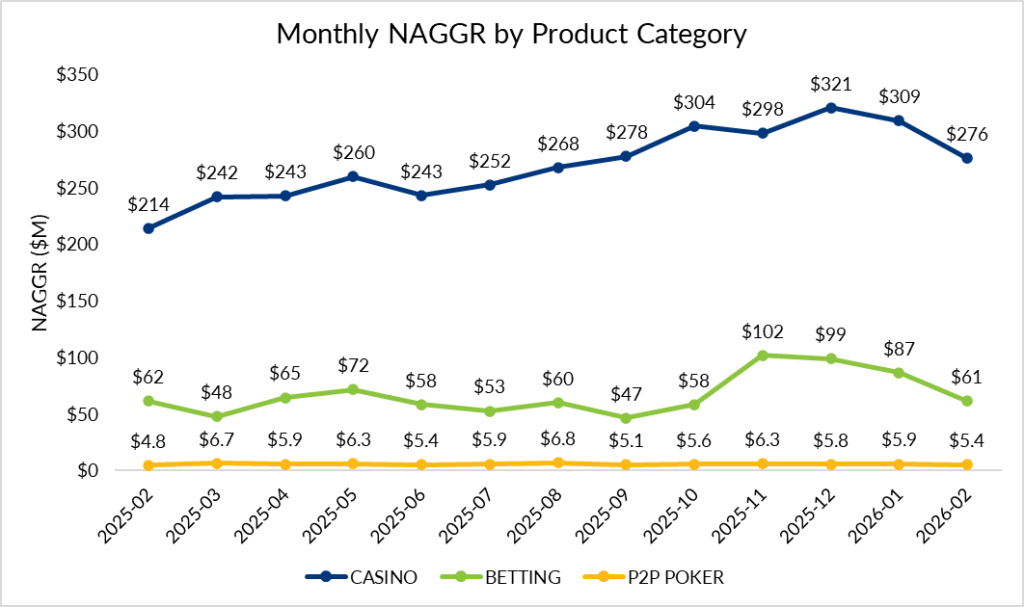

Those sports bets yielded $61.3m in operator revenue, almost exactly the same as the NAGGR made in the same month last year ($61.6m). Sports betting handle and revenue have tended to be pretty flat in terms of year-over-year growth in Ontario on a month-by-month basis, in a market in which online casino gaming consistently accounts for 85%-plus of regulated online gambling activity and around 80% of operator revenue.

In contrast to online sports betting, iCasino keeps posting strong annual growth.

While February’s online casino-specific handle was its lowest since September 2025, at $7.65bn, that represented a 26% jump from February 2025. Similarly, iCasino NAGGR climbed 29% from $214.0m last February to $275.7m last month, although once again that February 2026 total was the smallest since last September.

Peer-to-peer poker continues to account for a tiny sliver of the market. That vertical’s wagering activity ($135m) and revenue ($5.6m) were both lower than they were this time last year.

P2P poker is ring-fenced within Ontario, severely limiting its potential. The question of whether it can be opened up across international borders faces an appeal from several Canadian lottery corporations in the Supreme Court of Canada.

At the start of February, 48 licensed commercial operators were active in Ontario, running a total of 82 iGaming sites. Those numbers have both since dropped by one, as Rivalry announced midway through the month that it was suspending all play.

On the sports betting side, Ontario’s commercial sportsbooks faced increased competition in February as Ontario Lottery and Gaming (OLG) launched its expanded and upgraded sportsbook with its new platform provider Kambi in late January.

OLG online gaming activity is not included in iGO reporting. In early March, the crown corporation belatedly released its annual report for the fiscal year ended March 31, 2025, which showed that its revenue from online sports betting and online casino was $585m for that 12-month period.

Ontario’s online operators may soon have more competition. Other iGaming brands are expected to launch in the market soon, including sports streaming giant DAZN, which received a license to launch DAZN Bet in the province.